Today we will use R astsa (Applied Statistical Time Series Analysis) library to analyze data and predict it with ARIMA model.

Load the data

|

1 2 3 4 5 6 7 8 9 10 11 12 13 14 |

library(curl) library(quantmod) library(rusquant) library(xts) library(utils) # ASTSA lib is for ARIMA library(astsa) # Load the data price.ohlc <- getSymbols("SBER", from = Sys.Date()-1, to = Sys.Date(), src = "Finam", period = "1min", auto.assign = FALSE) price.cl <- Cl(price.ohlc) # Display close price on plot plot(price.cl) |

Look at ACF and PACF

Compare auto correlation and partial autocorrelation functions for diff data

|

1 |

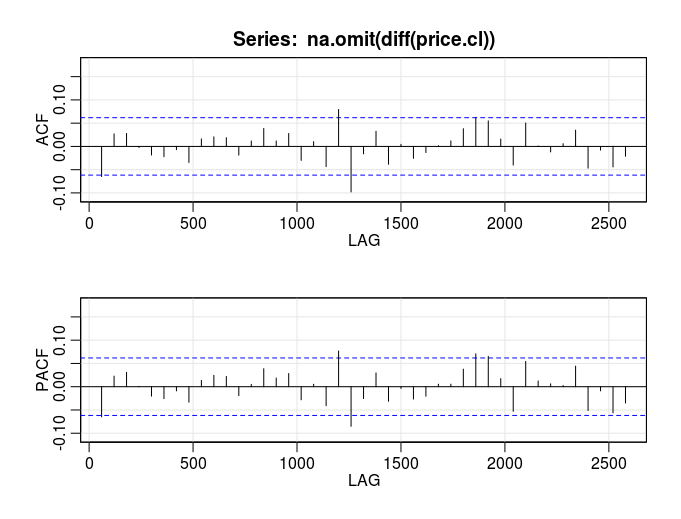

asf2(na.omit(diff(price.cl)) |

Output:

The ACF spikes are inside boundaries, it shows low auto correlation. Maybe ARIMA will not be a perfect model for that. Let’s look at first lags on PACF – only lag 1 spike is relatively big, so will use order 1 for ar (1,0,0) or ma (0,0,1).

Forecast

We need to choose (p,d,q) orders, where:

p – AR order

d– difference order

q – MA order

Let’s try Auto Regression model. PACF already showed us that only order 1 coefficients matter, so p = 1. We analyzing diff data, so d = 1. We don’t worry about MA in this example, so q = 0. Our (p,d,q) will be (1,1,0).

R code will be:

|

1 |

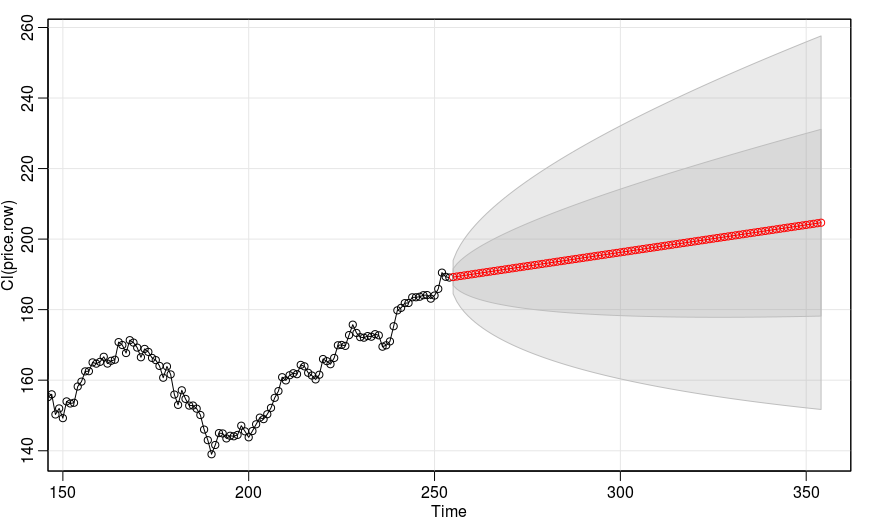

sarima.for(price.cl, n.ahead=100, 1,1,0) |

Output:

Where:

Black – original data

Red – prediction

Dark gray – 1 RMS prediction or 68% percentile

Light gray – 2 RMS prediction or 95 percentile.

Looks like a very broad prediction, so we need to try another model.

{kind=link}